Hot Rolled Coil (HRC) steel serves as a fundamental component in various industries, from automotive manufacturing to construction. Its pricing dynamics are influenced by a myriad of factors, including global economic conditions, trade policies, and supply-demand balances. Understanding these dynamics is crucial for stakeholders across the supply chain. In this article, we delve into the recent trends of HRC steel prices, analyze contributing factors, and explore the role of industry leaders like China Xino Group in navigating this complex landscape.

Recent Trends in HRC Steel Prices

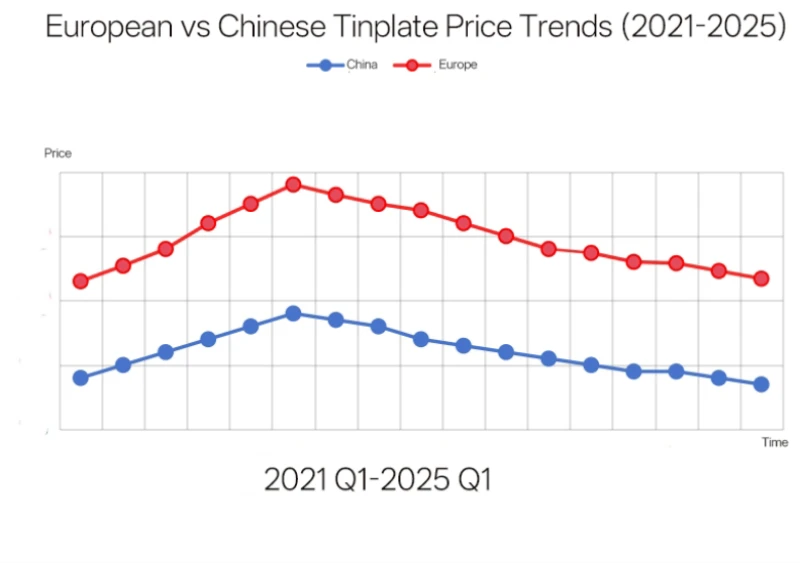

Over the past few years, HRC steel prices have experienced notable fluctuations. In 2021, prices soared to unprecedented heights, reaching an all-time high of $1,945 per ton in September. This surge was primarily driven by supply chain disruptions and a rapid rebound in demand post-pandemic.

However, this upward trajectory did not persist. By early 2025, prices began to stabilize. As of February 7, 2025, U.S. HRC prices stood at $719 per short ton, marking a 9.77% increase from their 2024 low in late July. This stabilization can be attributed to a combination of factors, including increased production capacities and moderated demand growth.

Factors Influencing HRC Steel Prices

Several key factors have played pivotal roles in shaping the pricing landscape of HRC steel:

Trade Policies and Tariffs: Governmental interventions, such as tariffs, significantly impact steel prices. For instance, the U.S. imposed a 25% tariff on steel imports as of March 12, 2025, leading to a spike in HRC prices to $949 per ton, up nearly 50% from previous levels. Such measures aim to protect domestic industries but often result in increased costs for downstream sectors.

Global Supply and Demand: The balance between steel production and consumption globally influences prices. In regions like India, the influx of cheaper Chinese steel imports has pressured local mills, leading to reduced operations and layoffs. Conversely, in the U.S., domestic producers like Nucor have implemented consecutive price increases for HRC products, reflecting a different market dynamic.

Raw Material Costs: Fluctuations in the prices of raw materials, such as iron ore and coking coal, directly affect steel production costs. For example, Australia's iron ore industry, pivotal for the national economy, confronts looming challenges and potential opportunities. The industry's revenue is projected to decline from $138 billion in 2023-24 to $102 billion by 2025-26, exacerbated by China's economic struggles and a potential recession.

Economic Indicators: Macroeconomic factors, including GDP growth rates, infrastructure spending, and automotive production, influence steel demand. In North America, steel demand is expected to rise in 2025, driven by increased automotive output.

Price Forecasts for 2025

Forecasting steel prices involves analyzing current trends and projecting future market conditions. Analysts have provided varied projections for HRC prices in 2025:

Wolfe Research: Managing Director Timna Tanners forecasts HRC to average $775 per short ton in 2025, suggesting a stabilization reminiscent of pre-pandemic levels.

S&P Global Commodity Insights: Analysts predict the average annual Midwest HRC price in 2025 to decline to $748 per short ton, down 3.5% from the estimated 2024 price of $778 per short ton.

WalletInvestor: This platform projects a bearish outlook, suggesting that HRC prices may drop from $890 per short ton to $751.68, indicating a potential decrease of approximately 15.5%.

Implications for the Steel Industry

The anticipated price trends have several implications for stakeholders:

Producers: Steel manufacturers may face tighter profit margins, prompting a focus on cost optimization and efficiency improvements.

Consumers: Industries reliant on steel, such as automotive and construction, could benefit from stabilized or reduced material costs, potentially leading to lower prices for end consumers.

Investors: Fluctuating steel prices necessitate careful analysis of market conditions, especially when considering investments in steel companies or related sectors.

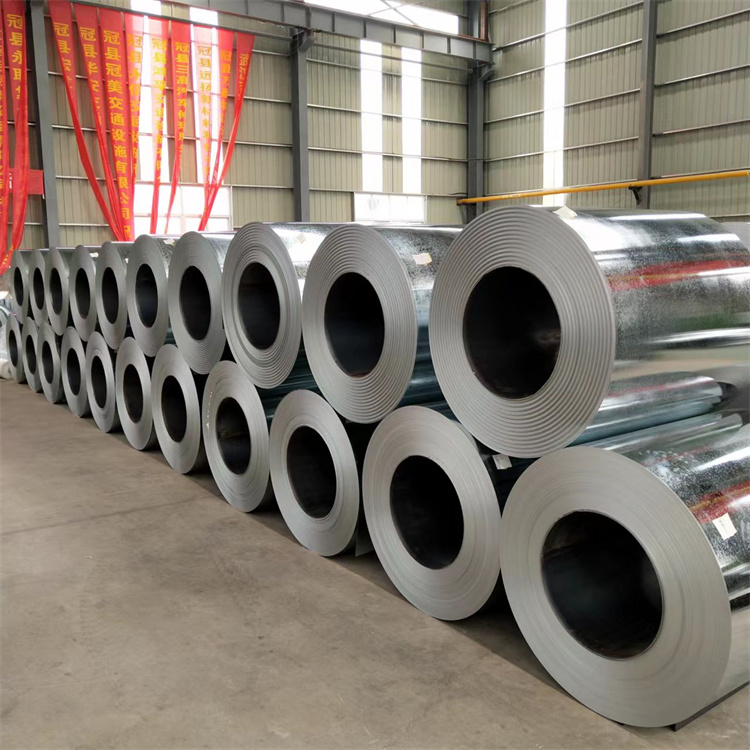

The hot-rolled steel coils shown in the picture are in a regular cylindrical shape, with a silver-gray color unique to metal on the surface. They are tied and fixed with steel strips, showing the solid texture of industrial products. As a key link in the steel industry chain, hot-rolled steel coils are widely used in construction engineering, automobile manufacturing, mechanical equipment and other fields due to their excellent strength and processing performance. They are an indispensable basic raw material for downstream deep processing.

Sustainability and Environmental Impact in the Steel Industry

As global industries increasingly emphasize sustainability, the steel sector is under growing pressure to adopt environmentally friendly practices. The production of HRC steel is highly energy-intensive, contributing significantly to carbon emissions. Leading steel manufacturers are investing in green technologies, such as hydrogen-based direct reduced iron (DRI) and electric arc furnaces (EAF), to reduce their carbon footprint. Additionally, stricter environmental regulations in key markets like the European Union and the United States are pushing companies to adopt cleaner production methods. The shift toward sustainable steelmaking not only benefits the environment but also enhances competitiveness in a rapidly evolving global market.

Strategic Adaptations for Future Market Conditions

To navigate the uncertainties of HRC steel pricing, businesses must adopt strategic adaptations, such as diversifying their supply chains, leveraging hedging mechanisms, and investing in digitalization for enhanced market insights. China Xino Group, for example, has taken proactive measures by expanding its production capacities while maintaining a strong focus on technological innovation. By integrating advanced manufacturing techniques and optimizing logistics, the company ensures resilience against price fluctuations. Moving forward, industry players that embrace innovation, sustainability, and strategic planning will be better positioned to thrive in an ever-changing steel market.

China Xino Group: Navigating the Steel Market

Established in August 2001, China Xino Group has positioned itself as a formidable player in the steel industry. With a registered capital of 150 million yuan and spanning 50 acres, the group has diversified its operations across various sectors, including steel products, metallurgical mineral resource processing, real estate development, chemical industry, and engineering technical services. This diversification strategy has enabled the group to mitigate risks associated with market volatilities.

One of its prominent branches, Qingdao Xino Steel & Iron Co., Ltd, specializes in coated steel products such as Galvanized Steel (GI), Galvalume Steel (GL), Pre-Painted Galvanized Iron (PPGI), Pre-Painted Galvalume (PPGL), Tinplate, and Tin-Free Steel (TFS/ECCS). With three main production bases housing six mills and a total of 24 production lines, the company boasts an impressive annual output of 1.5 million tons. This substantial production capacity underscores the company's commitment to meeting global steel demands.

Beyond production, Qingdao Xino Steel & Iron Co., Ltd has established a professional team dedicated to import and export activities to ensure that we can provide you with the best service.

745.webp)