Introduction

Tinplate coils, widely used in food packaging, beverage cans, and industrial applications, are a critical commodity in the global steel market. Europe and China are two major players in tinplate production and consumption, but their pricing strategies, cost structures, and market dynamics differ significantly.

This article compares tinplate coil prices in Europe and China, analyzes key competitiveness factors, and explores which market offers better value for buyers in the future .

Current Price Comparison

As of Q2 2024, the average prices for tinplate coils in Europe and China are:

Europe: $1,100–1,300 per ton (depending on thickness and coating)

China: $850–1,000 per ton (FOB basis)

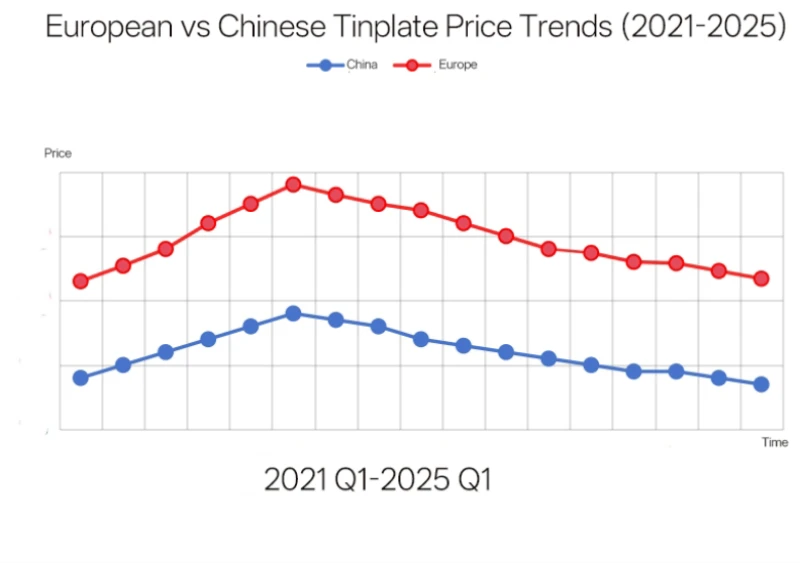

Price Trend Analysis (2022–2024)

China’s prices have remained 10–20% lower than Europe’s due to lower production costs and strong domestic supply.

Europe’s prices surged in 2022–2023 due to energy crises but stabilized in 2024 as gas prices eased.

China’s export prices face pressure from anti-dumping tariffs in some regions (e.g., Europe, the U.S.).

|  |

Comparison of Tinplate Coil Prices in European and Chinese Markets

Key Factors Influencing Price Competitiveness

1. Raw Material & Production Costs

| Factor | Europe | China |

|---|---|---|

| Iron Ore/Scrap | Import-dependent (Brazil, Australia) | Domestic supply + imports |

| Energy Costs | High (electricity, natural gas) | Lower (coal-based power) |

| Labor Costs | Higher wages | Competitive labor rates |

Europe suffers from high energy costs (post-Ukraine war) and strict carbon taxes.

China benefits from vertically integrated steel mills (e.g., Baowu Group) and cheaper coal power.

2. Supply & Demand Dynamics

Europe:

Declining local production (ArcelorMittal reducing capacity).

Increasing reliance on imports (Asia, Turkey).

China:

Overcapacity in steel production keeps domestic prices low.

Strong export demand from Southeast Asia and Africa.

3. Trade Policies & Tariffs

EU Carbon Border Tax (CBAM): Increases costs for imported steel, including tinplate.

China’s Export Policies: VAT rebates for steel exports were cut, slightly raising prices.

Anti-Dumping Duties: The EU has imposed tariffs on Chinese tinplate, reducing its price advantage.

4. Logistics & Supply Chain Efficiency

Europe: Higher inland transportation costs; reliance on seaborne imports.

China: Efficient port logistics (Shanghai, Ningbo) and competitive shipping rates.

Competitiveness Analysis: Europe vs. China

| Factor | Europe | China | Winner |

|---|---|---|---|

| Price | High ($1,100–1,300) | Low ($850–1,000) | China |

| Quality | Strict EU standards | Variable (top mills match EU quality) | Europe |

| Supply Stability | Dependent on imports | Self-sufficient + exports | China |

| Policy Risks | CBAM increases costs | Anti-dumping risks | Neutral |

Which Market is Better for Buyers?

For Cost-Conscious Buyers: China offers better prices, but tariffs may apply.

For High-Quality Demand: Europe ensures compliance with strict food-grade standards.

For Long-Term Contracts: Monitor EU carbon costs and China’s export policy changes.

Future Outlook & Recommendations

1. Europe’s Challenges & Opportunities

If energy prices drop further, EU mills may regain competitiveness.

CBAM will push European buyers toward local or green steel suppliers.

2. China’s Market Adjustments

Overcapacity may lead to price wars if demand weakens.

Export restrictions could tighten, raising global tinplate prices.

3. Strategic Buying Tips

✔ Short-Term: Source from China for best prices (check tariffs).

✔ Long-Term: Diversify suppliers (India, Southeast Asia emerging).

✔ Sustainability Focus: EU buyers may prefer low-carbon tinplate despite higher costs.

China Xino Group: Navigating the Competitive Landscape

Amidst these market dynamics, China Xino Group stands out as a formidable player. Established in August 2001 with a registered capital of 150 million yuan and spanning 50 acres, the group has diversified its operations across steel products, metallurgical resource processing, estate development, chemical industry, and engineering technical services. Its subsidiary, QINGDAO XINO STEEL & IRON CO., LTD, specializes in coated steel products, including galvanized steel (GI), galvalume steel (GL), pre-painted galvanized steel (PPGI), pre-painted galvalume steel (PPGL), and tinplate/TFS (ECCS). With three main production bases housing six mills and a total of 24 production lines, the company boasts an annual output of 1.5 million tons. This extensive capacity enables China Xino Group to offer high-quality products at competitive prices, catering to both domestic and international markets.

→ If you need anything, please feel free to contact us.

Conclusion

The competitiveness of tinplate coil prices between Europe and China is shaped by a complex interplay of production capacities, cost structures, and trade policies. While China's large-scale production often leads to lower prices, it also raises concerns about oversupply and market saturation. European producers, on the other hand, grapple with higher production costs and the challenges posed by imports. Companies like China Xino Group exemplify strategic positioning by leveraging extensive production capabilities and a diversified portfolio to navigate these market dynamics effectively.

745.webp)